Overview

Like many other jurisdictions, Malaysia has its own taxation system. Malaysia’s taxes are assessed on a current year basis and are under the self-assessment system for all taxpayers. All income accrued in, derived from, or remitted to Malaysia is liable to tax. That said, the income of any person (other than a resident company carrying on the business of banking, insurance or sea or air transport) derived [from sources] outside Malaysia and received in Malaysia is exempted from tax. One thing worth mentioning is Malaysia has an extensive number of double tax treaties available for the avoidance of Double Taxation.

Corporate Income Tax

In Malaysia, corporations are subject to corporate income tax, real property gains tax, sales and services tax (SST) and etc taxes. In other words, resident and non-resident organisations doing business and generating taxable income in Malaysia will be taxed on income accrued in or derived from Malaysia. Resident organisations carrying out business of air/sea transport, banking and insurance are taxable on their global income. Having said that, there are exemptions for resident banks, insurance companies, and Takaful companies [subject to specified conditions]. The tax year (or basis period) for a business usually follows the financial year ending in that particular year of assessment. For example, the basis period for YA 2017 for a business that closes its accounts on 31 December 2017 is the financial year ending 31 December 2017.

Tax filing could be very taxing if you are not familiar with it. You may read on to find more about the foreign-sourced income, corporate income tax rate, tax incentives and taxation for investment property in Malaysia so that you are well-informed of Malaysia’s taxation system. We provide a comprehensive guide and information that includes corporate tax planning as well as the assistance from professional accounting personnel.

Individual Income Tax

As the name implies, individual income tax in Malaysia is imposed on earned in Malaysia or received in Malaysia from outside Malaysia. In this light, every individual is subject to tax on income accruing in or derived from Malaysia. That said, income earned overseas (remitted to Malaysia by a resident or individual) is exempted from tax. Income is assessed on a current year basis and individuals must comply with the self-assessment scheme. The tax rate differs as it is calculated according to the chargeable income of resident individual taxpayers.

If you are new to Malaysia’s taxation system, be it the corporate tax or the personal income tax, we are here to help you to understand the taxation system and do the tax filing.

It is important to know what will happen to a company if a company fails to submit Form CP204 within the stipulated period, Form CP204 submitted but fails to pay the tax instalment or under-estimated tax payable for a particular year of assessment. Each offence may result in a penalty ranging from RM200 to RM2,000 being charged by LHDN.

The most commonly asked question by our clients in filling up the Form CP204 is: How to calculate tax estimate for CP204?

In order to calculate the possible tax payable for the coming year, the company must make several assumptions and projections based on the current year’s management results. It is important to predict what will happen based on what is having now.

The Inland Revenue Board (IRB, or commonly known as LHDN, Lembaga Hasil Dalam Negeri) has issued a notice to all professional associations on 9 June 2011 for the clarification of submission requirements for CP204.

Small & Medium Companies are advised to submit CP204

IRB has in its letter informed all companies to submit its tax estimation (CP204) for avoiding any possible unnecessary penalty due to administrative issues, even though these companies are not required to submit CP204.

Under the self-assessment system, every company is required to determine and submit in a prescribed form (Form CP204) an estimate of its tax payable for a year of assessment, 30 days before the beginning of the basis period.

A new company must submit CP204 within 3 months once started a business

However, when a company first commences operations (ie during the first period), the estimate of tax payable must be submitted to the IRB within 3 months from the date of commencement of its business and thereafter no later 30 days before the beginning of the basis period.

Under the Self Assessment System, the burden of computing the taxpayer’s liability is shifted from the Inland Revenue Board (IRB) to the taxpayer and accordingly, taxpayers are expected to compute their tax liability based on the tax laws, guidelines and rulings issued by the IRB.

The Income Tax Returns (Form C) submitted by the companies will no longer be subject to a detailed review by the IRB.

The main objective of the Self Assessment System is to inculcate a practice of voluntary compliance by the taxpayers and at the same time reduce the workload of the IRB to enable them to concentrate on areas which have a high tax risk and a potentially significant loss in revenue.

The implementation of the self-assessment system has also resulted in changes to the tax compliance cycle and the penalty provisions. These changes are explained in greater detail below.

Under Self Assessment System, tax audits will be IRB’s key enforcement tools to ensure that the tax returns submitted are correct and have been prepared in accordance with the provisions of the laws, guidelines and rulings issued by IRB.

Essentially, an audit is an examination of a taxpayer’s records to ensure that the income and tax liability declared to the IRB in the Income Tax Return are true, correct and comply with the tax laws and rulings.

IRB carries out 2 types of audits, namely Desk Audit and Field Audit.

The Desk Audit will involve the review of documents or information obtained by correspondence and interviews at the IRB’s offices whilst the Field Audit would entail a visit to the taxpayer’s premises for a detailed review of all relevant documents.

Cases for audit are selected through the computerised system based on risk analysis criteria and on various criteria such as business performance, financial ratios, type of industry, past compliance records, third party information, etc.

Once a taxpayer is selected for an audit, the IRB will inform the taxpayer via a telephone call followed by an official notification letter sent via mail or fax.

The period between the date of notification and the audit visit is 14 days. A shorter period of notification may be fixed by IRB with the consent of the taxpayer.

The scope of a tax audit under the self assessment system normally covers a period of 1 to 3 years, unless there are valid reasons to go beyond that period. The time frame for the conclusion of a tax audit is normally within 3 months.

Upon the completion of an audit, the IRB will issue a tax computation summarising the tax adjustments based on their findings and subsequently an additional assessment to collect the additional taxes from the taxpayer.

The taxpayer may still appeal against this assessment by submitting the appeal, through the prescribed Form Q to the Special Commissioners of Income Tax within 30 days from when the assessment is raised.

With effect from 1 Jan 2014, the time-bar for tax audits is reduced from 6 years to 5 years.

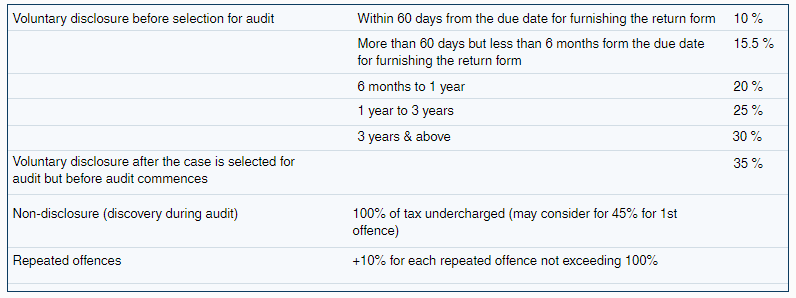

(a) Penalties for omission/non-disclosure

Under the tax audit system, the IRB has also introduced a new penalty regime for non-disclosure and omission of information that affects a taxpayer’s tax liability. The penalty regime is summarised as follows:

.

(b) The penalty for not providing reasonable facilities and assistance

Based on Public Ruling 7/2000, failure by a taxpayer to provide reasonable facilities and assistance to the IRB when conducting an audit is an offence and upon conviction, the taxpayer may be liable to a fine of between RM1,000 to RM10,000 or face imprisonment for a term not exceeding 1 year or both.

(c) Failure to keep sufficient records

The company or persons responsible, upon conviction, will be liable to a fine of between RM200 to RM2,000 or face imprisonment for a term not exceeding 6 months or both.

At Business Advisory services we are know for our accounting and taxation service in the Klang Valley and the rest of Selangor. If you would like to know more about our tax services please feel free to contact us.